Gold in 2026: Records, Sharp Corrections, and Renewed Safe-Haven Momentum – A Professional Commodities Perspective as of February 23

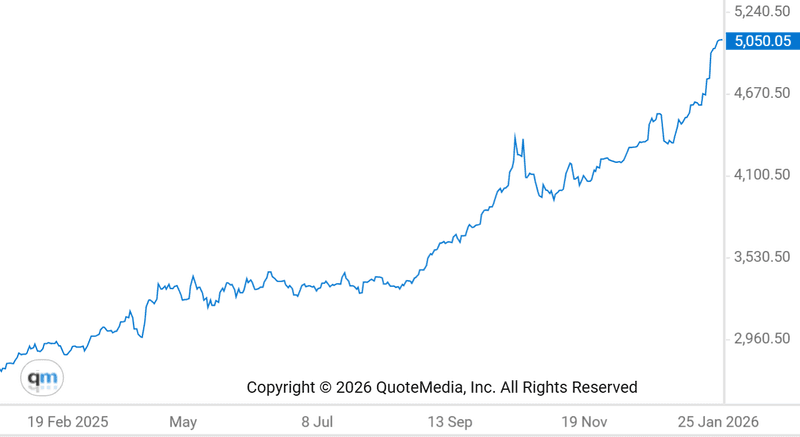

The opening weeks of 2026 have delivered one of the most volatile—and ultimately affirming—starts on record for gold. Spot gold is currently trading at $5,206 per ounce (as of February 23, 2026, per Trading Economics and live market data), up nearly 2% on the day and reclaiming multi-week highs. This follows an all-time high of $5,608.35 hit in late January, a brutal late-January/early-February correction that shaved more than 15% off the price at its worst, and a resilient rebound driven by fresh trade-policy uncertainty.

To put the year-to-date move in context: Gold entered 2026 already elevated from its extraordinary 2025 rally (up roughly 55-70% that year, depending on the exact endpoint). It has since added another ~18-20% amid extreme swings—classic behavior for an asset repricing structural demand shifts in real time.

(Above: Gold’s longer-term ascent through early 2026, followed by the sharp January-February 2026 volatility in focus—peak near $5,600, correction into the $4,200s-$4,900s range, and recent recovery.)

January 2026: The Record-Breaking Surge

Gold didn’t ease into the new year—it exploded. By January 26, spot prices had surged past $5,100 for the first time ever, extending a multi-year bull market fueled by:

- Persistent central-bank buying (863 tonnes in 2025, with forecasts now at 950+ tonnes for 2026).

- Heightened geopolitical tensions, including tariff saber-rattling and regional flashpoints.

- Fiscal-sustainability concerns in major economies and ongoing de-dollarization trends.

The metal closed January with multiple all-time highs, peaking at $5,608 around January 28-29. Adjusted for inflation, this surpassed the 1980 peak in real terms. Demand was broad-based: official-sector accumulation, ETF inflows, and retail investors rotating into hard assets amid uncertainty. For commodities professionals, this wasn’t speculative froth—it reflected gold’s re-rating as a core portfolio diversifier in a world of elevated macro and policy risks.

Late January–Early February: The Sharp Correction

The party paused abruptly on January 30 when President Trump nominated former Fed Governor Kevin Warsh as the next Federal Reserve Chair. Markets interpreted Warsh—a credible, institutionally minded figure with hawkish leanings on balance-sheet normalization—as a signal of restored Fed independence and potentially tighter policy than feared.

The reaction was visceral:

- Gold plunged as much as 11-15% in hours (its steepest single-day drop since 1983 in some sessions).

- Silver cratered over 30%.

- The U.S. dollar strengthened modestly, and Treasury yields ticked higher.

By early February, prices had retreated toward the $4,400–$4,900 zone. Margin hikes on futures contracts added technical pressure. Many commentators called it a healthy “reset,” but for physical-market participants it underscored gold’s sensitivity to shifts in monetary-policy expectations.

Mid-to-Late February: Rebound on Tariff Uncertainty

The correction proved short-lived. On February 20, the U.S. Supreme Court struck down key portions of the Trump administration’s broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA), ruling 6-3 that the president had overstepped congressional authority on tariffs.

The administration quickly responded by announcing replacement measures—a 10% (later hiked to 15%) global tariff under alternative authorities, set to take effect imminently. The result? Renewed trade-war jitters, a softer dollar, and immediate safe-haven flows back into gold.

By February 23, the metal had climbed to three-week highs above $5,200, supported by:

- Lingering uncertainty over trade deals and retaliatory risks (EU and India signals already emerging).

- Softer-than-expected U.S. economic data reinforcing expectations for Fed rate cuts later in 2026.

- Continued central-bank and Asian physical demand.

This rebound highlights a recurring 2026 theme: policy volatility is gold’s friend when it raises questions about global trade stability and currency reliability.

The Structural Fundamentals Remain Bullish

Beyond the headlines, three pillars continue to underpin gold’s higher trading range:

- Central Banks as Structural Buyers — Purchases are no longer cyclical but a deliberate diversification away from dollar-heavy reserves. Consensus estimates point to 800–950 tonnes annually through 2026.

- Portfolio Reallocation & Debasement Hedge — With sovereign debt loads elevated and fiscal debates ongoing, institutional and retail allocators are increasing gold exposure for diversification. ETFs are forecast to see strong inflows.

- Macro Backdrop — Lower-for-longer real rates (even if nominal policy is steadier under a Warsh-led Fed), persistent inflation risks in certain regions, and geopolitical fragmentation all favor non-yielding stores of value.

Analyst forecasts reflect this resilience. JPMorgan sees average prices near $5,055/oz in Q4 2026 (with upside to $6,000 longer-term). UBS eyes potential for $6,200 mid-year before consolidation. Bank of Montreal’s bull case now reaches $6,500. Even more conservative houses have hiked targets materially since late 2025.

Professional Takeaway for Gold Market Participants

2026 has already demonstrated that gold’s bull market is not linear—but it is durable. The January peak and February correction were textbook examples of event-driven volatility overlaying powerful secular demand. The latest rebound on trade friction reinforces that gold thrives when policy uncertainty rises, not despite it.

From a commodities standpoint, the risk/reward remains skewed higher. Support levels near $4,800–$5,000 have held impressively; resistance at the prior $5,600 ATH will be tested again if macro or geopolitical catalysts intensify. For those focused on the physical market—whether through bullion, mining equities, or related assets—the message is clear: volatility creates opportunity, but the underlying bid from official and investor demand provides a floor far above pre-2024 levels.

Gold isn’t just “in the news”—it is reasserting its role as the ultimate monetary insurance policy in an increasingly fragmented world. As we move deeper into 2026, expect continued two-way price action, but with a structural bias that favors the upside.

Stay vigilant on Fed communications, trade developments, and central-bank reserve data. The yellow metal has delivered for those who understood its evolving fundamentals—and 2026 so far suggests that story is far from over.

(All prices and events referenced are current as of February 23, 2026 market data. Past performance is not indicative of future results. This is for informational purposes and not investment advice.)

No comments

0 comments