Gold & Geopolitics

Gold & Geopolitics

As featured in the Jan/Feb 2024 issue of Gold Prospectors Magazine

By: Gino D’Alessio

UNDERSTANDING THE INTERPLAY BETWEEN GOLD MARKETS AND

GLOBAL EVENTS

I’m sure you’ve read many times how gold has been valued throughout the millennia as a store of value and a medium of trade. So, I’ll skip the exact details of how we came about to value gold the way we do.

Just to add that, while gold’s worth and importance are just as strong today as they have ever been, the true value of gold had been capped for decades by the U.S. administration through the convertibility of gold. This legislation effectively placed a false price on the value of gold and kept it at unrealistic levels until 1971.

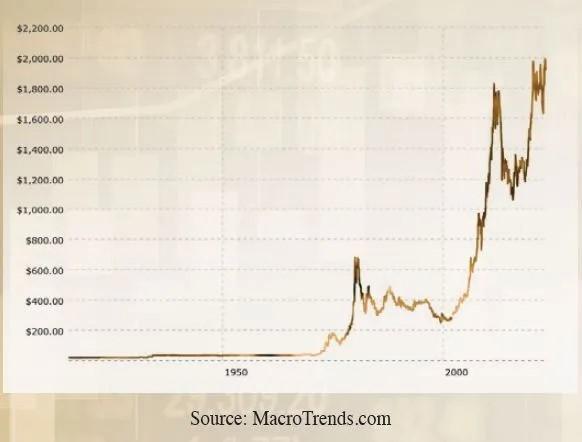

In August of that year, President Richard Nixon dropped the gold standard and allowed the price of gold to float according to free-market rules, which are those of supply and demand. Before Nixon suspended the convertibility of gold, an ounce of the shiny metal was valued at around $43 U.S.

We can see from the chart below the progression in the price of gold per ounce from August 15, 1971, to the current day. With this in mind, we’re about to investigate how global events, including geopolitics and central bank policies, have an impact on the price of gold.

GOLD’S ROLE IN THE MODERN ECONOMY

To get a better understanding as to why gold would react to global geopolitical events or central bank policies, let’s understand gold’s current role in the modern economy.

From being a medium to facilitate the exchange of goods and wealth, gold has also gained other functions in modern times. The precious metal is used as a reserve commodity by most of the largest and wealthiest countries in the world.

In the past few decades, gold has also become a necessary resource to produce a variety of electronic components and devices. This new role for gold has further pushed its valuation and desirability beyond wealth storage and jewelry.

And lastly, but not to be underestimated, is gold’s role as a refuge asset. When financial and societal crises appear, gold is considered a safehaven asset. At the same time, when the future’s looking bright, gold will often be overlooked in favor of traditional investments.

We can see that due to these factors, gold prices may react to various scenarios, whether they be geopolitical risk, economic activity, or central bank policy.

GOLD RESERVES AS AN INDICATOR OF ECONOMIC STRENGTH

Gold has been kept by the world’s largest economies for centuries, with the remarkable exception of Canada, which sold all its gold reserves in 2016. Despite the decision of Canada, countries like the U.S., Germany, Italy, and China have thousands of tons of the precious metal.

The pie chart below shows gold reserves per country in tons as of Q1

2023. We can see clearly by the quantity of gold held in reserve that Western countries place a high level of importance on this commodity. More importantly, two countries that are emerging in international politics have been amassing gold reserves over the past 10 years.

The specific reasons for the accumulation of gold are officially unknown. However, it’s reasonable to believe that these countries wish to enhance their positions as suppliers of global currencies, just like the major economies that have thousands of tons.

Think of the United States with more than 8,000 tons and considered the world’s reserve currency. It takes more than gold. In fact, the U.S. has the world’s largest economy, but these countries, especially China, are also growing rapidly.

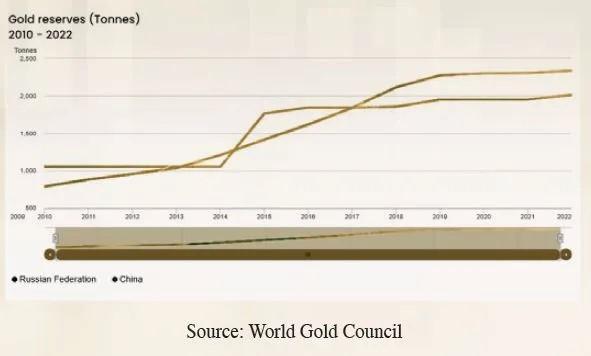

China and Russia have been stocking up on gold at a faster pace than any of their competitors. According to the World Gold Council, China held 1,054 tons of gold in 2010, while Russia held 788 tons. China has more than doubled its gold reserves, while Russia has nearly tripled them.

The chart above shows the rapid growth of accumulation in gold reserves for Russia and China since 2010.

GOLD AS AN INDUSTRIAL RESOURCE

Gold in the past 20 to 25 years has taken on an ever more important role as a primary material for use in a wide variety of industrial sectors, including electronic devices, dentistry, the space industry, catalytic converters, and fuel cells.

Approximately 80% of industrial gold demand comes from the electronics sector. The fact that this industrial sector is likely to grow further should maintain or increase current levels of industrial demand.

According to the World Gold Council, the technology sector represents 6.5% of gold demand. As the demand for electronic devices continues to grow, we may expect this to create more demand for gold, all things being equal.

Bearing this in mind, supply gluts in semiconductor production can cause a decrease in demand and possibly reduce the price of gold if the lack of demand is not met by an increase from other sectors.

GOLD AS A HEDGE AGAINST INFLATION AND CURRENCY DEPRECIATION

Gold has been known to consistently perform well during times of inflation or currency depreciation. Inflation has a negative effect on buying power; as prices go up, you can buy fewer things for each dollar.

Gold holders clearly know this and will want more dollars to compensate for the reduction in purchasing power. This is due to the fact that gold seldom loses its value to gold holders. Other factors come into play, creating imbalances between supply and demand that can decrease the price of gold.

However, in general terms, all else being equal, gold holders will expect to receive more of a currency that is worth less. The chart below shows the price of gold per ounce and U.S. inflation since 1971. The pink rectangles highlight how often gold prices have increased as the inflation rate also rose.

Out of eight bouts of rising inflation, six of them coincided with higher gold prices, while only on two occasions did gold prices drop (green highlights). We can see that the correlation between higher and expanding inflation and higher gold prices seems very strong.

CENTRAL BANK MONETARY POLICY

When inflation rises above the Federal Reserve’s target inflation rate, it must take action to bring inflation back under control. Inflation control is one of the central bank’s two mandates: Inflation and full employment.

However, to bring inflation down, the Federal Reserve has no choice but increase interest rates and tighten the money supply. Eventually, the economy will cool down, and inflation will decrease. Higher interest rates are good for some investors, but for gold markets they tend to spark a decrease in price.

This fall in the value of gold is usually temporary, as some gold investors switch to other assets, such as bonds, which offer a fixed income stream and are more attractive when interest rates are higher.

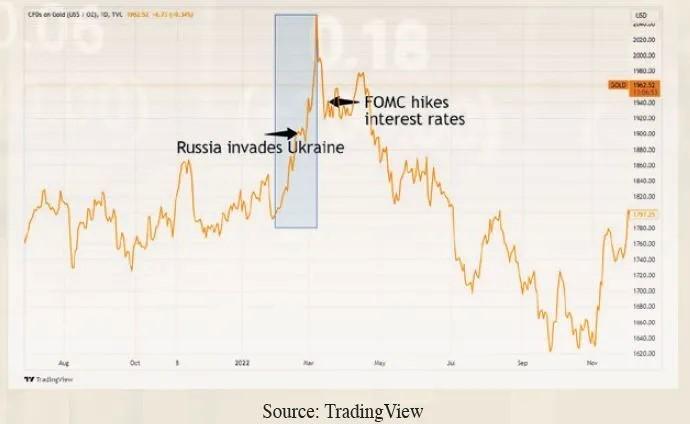

The chart above shows the price of gold and the Fed Funds rate, which is usually in between the range set by the Federal Reserve. In March 2022, the central bank raised interest rates for the first time in several years. Inflation had already peaked above 8 percent the month before.

The financial markets began anticipating a rapid drive by the Federal Reserve to tighten monetary policy and increase interest rates rapidly. Gold markets, like most financial markets, overreacted and, as the months went by, fell to around $1,600 per ounce by September.

Shortly after that, in November, the gold market sensed that the central bank policy might be changing, and a pivot was about to happen. The socalled pivot refers to a change in monetary policy from tightening to loosening. And, of course, gold prices started to rise again since then, in conjunction with a slower pace of interest rate hikes.

The Ukraine-Russia Conflict & Higher Bond Yields

The beginning of 2022 was an interesting period for gold markets from the point of view of market dynamics. The threat of war toward the end of January had already sparked a rally in gold prices. The bull run was further extended when Russia actually invaded Ukraine.

But there was another issue going on at around the same time: Federal

Reserve monetary tightening. At the FOMC (Federal Open Market Committee) meeting in March, the committee decided to hike interest rates by 0.25%. Gold prices took a small dive, but geopolitical fears of an escalation of the war in Eastern Europe kept gold prices bouncing around the $1,940 level.

Eventually, the factor of higher interest rates and higher bond yields put enough pressure on gold prices to send them lower again. Gold prices reacted to the fear of war spreading beyond the Eastern European theatre. However, the higher bond yields eventually took over, and gold prices took a nosedive, finding a bottom around $1,620 in September.

THE FINANCIAL CRISIS OF 2008

The causes of the financial crisis in 2008, which was one of the worst in history, have not been adequately exposed, in my opinion. A good explanation might come from the film “The Great Short.” However, it’s not the objective of this article to establish the catalyst of the crisis. But I would say it was due to multiple factors of neglect and lousy banking policies.

The 2008 crisis really started in Q2 2007, when the broad stock market started faltering. The S&P 500 returned 3.6%, while gold prices rose

32.8%. The following year the crisis hit the markets in the U.S. and the world in general; the S&P 500 fell by 36% while gold prices returned 2.4%.

By the time the financial markets had reached a bottom in March 2009, the S&P 500 had fallen by 56.8% from its high in October 2007. Whereas gold had a positive performance in the same time frame going from $735 to $895 for an increase of 21.7%.

The chart above shows the performance in returns for the S&P 500 and gold from Q2 2007 to Q2 2009. The difference in returns between the two markets equals 79.9 percentage points.

The financial crisis of 2008 was deep and severe, but gold had a remarkable performance when compared to stocks and bonds. Gold’s performance was probably more noticeable in the 2008 crisis due to the depth of the stock market sell-off.

Yet in 2020, gold also held its ground and outperformed the S&P 500 during the global pandemic. In 2020, at the start of lockdowns, the S&P dropped 36%, while gold lost 12%. However, the full-year performance of the S&P 500 was a return of 14.4%, while gold on the other hand gained 26.1%

SCARCITY OF GOLD AND MONEY

Another driver of gold prices is its relative scarcity. Supply is primarily limited by the capacity of mining companies to extract the precious metal at a cost that is low enough to make a profit.

What happens then when gold prices go down too much? Gold miners stop mining. If they can’t extract gold for a profit at current market prices, gold supply slowly comes to a halt. This creates an imbalance between demand and supply and eventually pushes gold prices back up again.

If we compare that with how the money supply works, we see the complete opposite. The Federal Reserve can print as much money as needed with no oversight from Congress. Or, as I would put it, with Congress’ full blessing.

The central bank can expand the money supply to stimulate economic activity and pay for government debt. If the economy overheats, it simply puts interest rates higher, constraining economic activity.

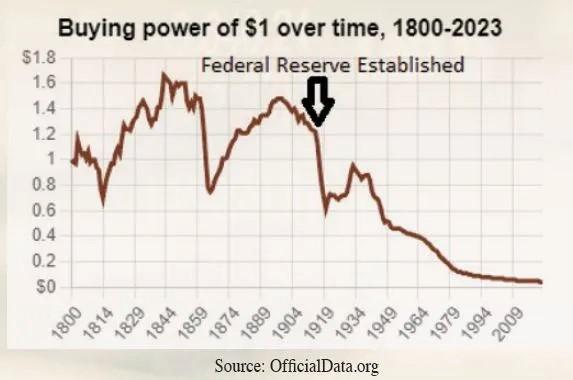

The chart above shows the purchasing power of the U.S. dollar since 1800. We can see there are two distinct parts of the chart: one previous to the establishment of the Federal Reserve and the other after the Federal Reserve was established.

Considering modern times, basically from the advent of the central bank, we can see how the dollar has consistently lost value over time. During most of this time, the value of gold was pegged by the U.S. administration.

From August 1971, when the convertibility of dollars to gold was dropped, the value of gold has only risen. We can fully see the effect of pricing gold against a medium that is worth less and less over time; gold holders will demand more of that medium.

CONCLUSION

We have seen how gold’s price intertwines with geopolitical events and monetary policy. And also, how demand increases or decreases as a reaction to changes in inflation and bond yields. New roles for the yellow metal have also created another demand factor, which will influence the price of gold as the demand for a number of products varies.

For decades before 1971, the price of gold used to be fixed by Congress and clearly didn’t reflect its true value. Since the gold standard was dropped, we have seen the price of gold, with considerable fluctuations, continue to grow.

The war in Ukraine sparked by Russia’s invasion of the country also showed how gold is resilient and can gain value even in times of risk of war or possible catastrophic events. This is due to the refuge value investors see in gold as an asset of last resort.

Considering the limited increase in the supply of gold when compared to the unlimited supply of fiat money, we can also realize that the value of gold should continue to grow. As the dollar’s value continues to decline, more units of dollars would be necessary to compensate a holder of gold.

Finally, the gold hoarding that countries like China and Russia have been practicing over the past 10 years leads me to believe that there are reasons strictly related to monetary credibility and geopolitical positioning.

Gino D’Alessio is an OTC dealer-broker in the financial markets, having traded bonds, derivatives, and foreign exchange. Since 2015, he has been writing about alternative investments. He brings more than two decades of experience.

No comments

0 comments